What are your priorities for retirement?

Click on each priority to learn more.

Enjoy more time with my family

Having more family time is a great way to spend your retirement.

But have you thought about how that could change if you have an unexpected health event?

Make sure my retirement income lasts

It’s important to make sure you have enough retirement income to last.

But have you thought about how your retirement income would be affected if you have an unexpected health event?

Spend more time on my hobbies

Spending time on hobbies is a great way to spend your retirement.

But have you thought about how those hobbies could change if you have an unexpected health event?

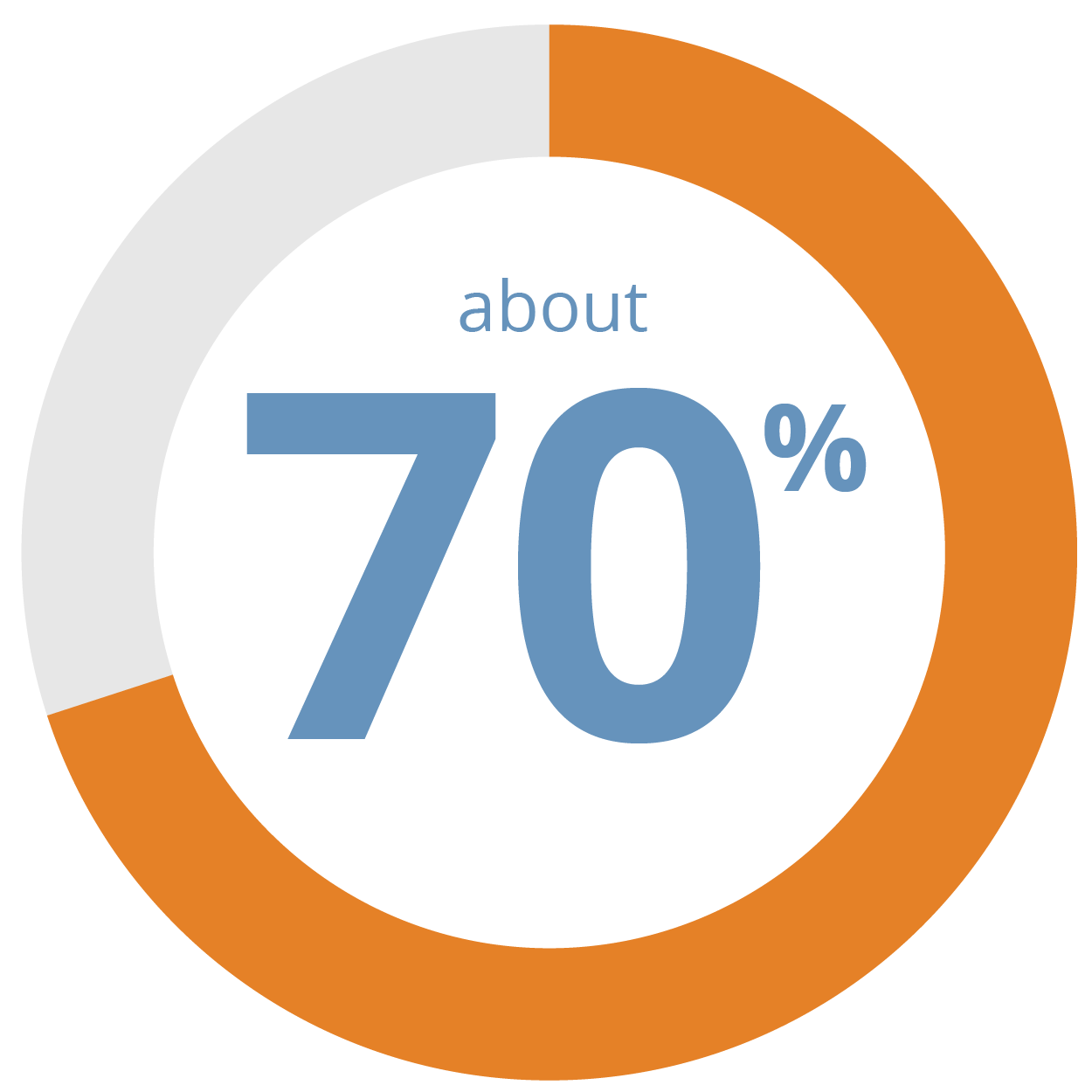

of people turning 65 today may need some type of long-term care in their future.

“Who Will Provide Your Care?” LongTermCare.gov. U.S. Department of Health and Human Services. https://longtermcare.acl.gov/the-basics/how-much-care-will-you-need.html. Last modified: 10/10/2017

of those requiring care will need it for longer than 5 years.

“How Much Care Will You Need?” LongTermCare.gov. U.S. Department of Health and Human Services. https://longtermcare.acl.gov/the-basics/how-much-care-will-you-need.html. Last modified: 10/10/2017

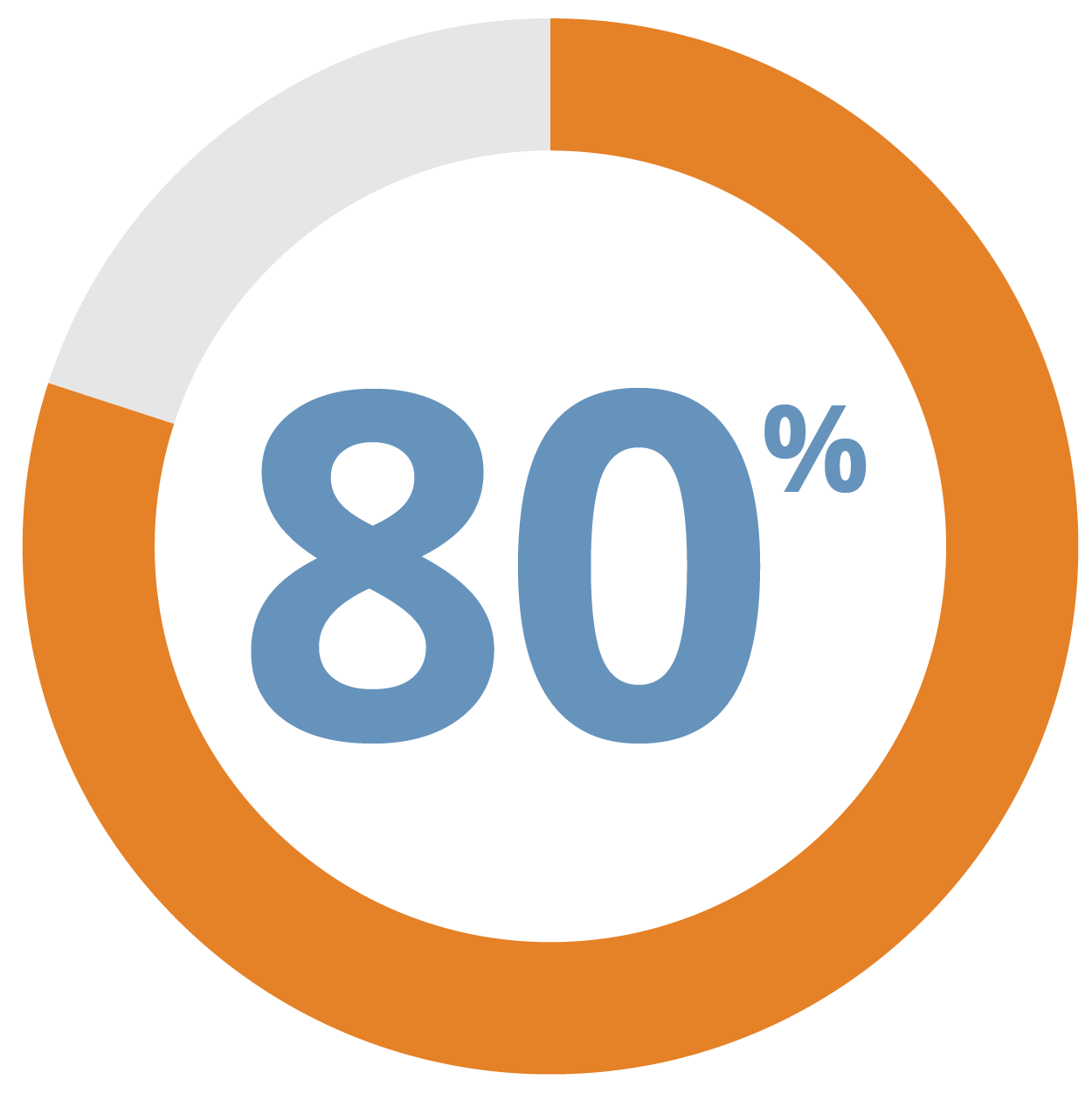

of care at home is provided by unpaid caregivers.

“Who Will Provide Your Care?” LongTermCare.gov. U.S. Department of Health and Human Services. https://longtermcare.acl.gov/the-basics/how-much-care-will-you-need.html. Last modified: 10/10/2017

Why long-term care protection?

Control your care

Taking steps now to prepare, before you need care, can help you maintain control over your options in the future.

Preserve your assets.

Knowing that you’ve planned now may ensure that a long-term care need won’t impact your retirement assets.

Protect your family

Planning for care now allows your friends and family to be there for you—instead of having to become your caregiver.

In-Home Care

Homemaker Services:

$51,480

Home Health Aide:

$52,624

Community & Assisted Living

Adult Day Health Care:

$19,500

Assisted Living Facility:

$48,612

Nursing Home Facility

Semi-Private Room:

$90,155

Private Room:

$102,200

Source: https://www.genworth.com/aging-and-you/finances/cost-of-care.html,

Genworth Cost of Care Survey 2019, conducted by CareScout®, June 2019

Asset Care isn’t traditional long-term care insurance

It combines whole life insurance with long-term care protection. Unlike traditional long-term care policies, your premiums will never increase and they won’t go to waste if you never need care. Instead, your policy death benefit is paid to whomever you choose.

Let’s Talk

Details

Click for the answers to five most asked questions.

How can I fund Asset Care?

Can one policy protect me and my spouse?

What types of services will Asset Care cover?

How long will I be protected?

What happens if I never need long-term care?

How can I fund Asset Care?

You can fund your Asset Care policy numerous ways. You can use funds from your 401(k), IRAs, annuities or other exisiting accounts. You can choose to pay in one lump sum or over time.

We can customize a solution that works for you and your family.

Can one policy protect me and my spouse?

With our joint protection option, you and your spouse won’t need to purchase individual policies or try to manage two sets of benefits. Even if you both need care at the same time, we make it easy by covering you both under one policy with shared benefits.

What types of services will Asset Care cover?

Asset Care can help you pay for almost any level of care, from minimal but meaningful social care to comprehensive residential care:

|

|

How long will I be protected?

Long-term care needs are unpredictable. It’s impossible to know when you’ll need care and for how long. Asset Care is the only whole life product to offer a protection option for the extent of a lifelong condition—like Alzheimer's or dementia.

What happens if I never need long-term care?

Because Asset Care is based on whole life insurance, any amount that you don’t use on long-term care expenses becomes a death benefit that can be paid to whomever you choose.

Our customers have placed their trust in the companies of OneAmerica for more than 140 years.

We’ve been a pioneer in the long-term care marketplace for more than 30 years.

We show up every single day to focus on your needs, so you can focus on the needs of those that mean the most to you.

Ready to take the next step?

Reach out to your financial professional, and let them know you'd like to discuss your retirement priorities and how long-term care protection can play a part.

Note: Products issued and underwritten by The State Life Insurance Company® (State Life), Indianapolis, IN, a OneAmerica company that offers the Care Solutions product suite.

Asset Care Form number: ICC18 L302, ICC18 L302 JT, ICC18 L302 SP, ICC18 L302 SP JRICC18 R537, ICC18 R535, ICC18 R532, ICC18 R539, ICC18, R538, ICC18 R533 and ICC18 R540.

Not available in all states or may vary by state. Asset-based products allow prepayment of the death benefit for qualifying long-term care expenses through life insurance, annuities or life insurance and annuity combination. Some products may have surrender charges and elimination period. All guarantees are subject to the claims paying ability of State Life. All individuals in the scenarios. Examples presented are fictitious and all numerical examples are hypothetical and are used for analytical purposes only. Provided content is for overview and informational purposes only and is not intended and should not be relied upon as individualized tax, legal, fiduciary, or investment advice. The policies and long-term care insurance riders have exclusions and limitations. For cost and complete details, contact your insurance agent or company.

In Texas: The Senior Counseling Notice (HICAP) is required at solicitation: A Senior Insurance Counseling Program is available to you free of charge. Health Information Counseling and Advocacy Program (HICAP), 701 W. 51st W-352, Austin, TX 78751. 1-800-252-9240.

The purpose of this marketing material is the solicitation of insurance, and contact will be made by an insurance agent or insurance company.